Hidden away in the 2017 Tax Cuts and Jobs Acts is a program called the Investing in Opportunity Act, which can bring much needed investment to some of the nation’s distressed communities. It allows for investment in new businesses and in education, particularly charter schools and skill trainings programs.

It is gaining popularity as a new real estate development program because investors benefit by being allowed to re-invest their capital gains (no amount too small or too large) into a recognized Opportunity Zone. The advantage is the ability to defer tax, or in some cases permanently exclude part or all of the tax on their capital gain invested as well as the gain earned on their investment into the Opportunity Zone.

The IRS has just issued proposed regulations that provide guidance and clarity to the uncertainties surrounding the requirements that must be met in order to defer the recognition of gains. The proposed regulations provide clarity regarding:

- Eligible gains

- Eligible taxpayers

- Electing post-10-year gain exclusion if zone designation expires

- Deadline for electing post-10-year gain exclusion

- Safe harbors for statutory qualifying property tests

- Definition of substantially all

The investment can be passive or active depending on the investor’s ability to locate, identify and execute an Opportunity Zone project. Investors will have the ability to pool their money together with other investors in an Opportunity Fund. “Many investors are willing to provide the capital, but lack the wherewithal to locate and execute investment opportunities in communities that need it”, says the Economic Innovation Group.

How do you get started? Familiarize yourself with the following and how they work together to stimulate investment:

- Qualified Opportunity Zone (QOZ)

- Qualified Opportunity Fund (QOF)

- Qualified Opportunity Zone Property (QOZ Property)

- Qualified Opportunity Zone Business (QOZ Business)

Qualified Opportunity Zones are an economic development tool designed to revitalize distressed communities and create jobs. States were required to nominate low-income communities as Qualified Opportunity Zones and submit their nominations to the Secretary of Treasury by April 20, 2018 for certification.

Each designated QOZ shall remain in effect from the date of designation to the close of the 10th calendar year beginning on or after the designation date. Based on current legislation, all QOZs designated by the June 18th deadline must terminate no later than December 31, 2028.

The IRS recently issued a bulletin publishing all of the population census tracks that the Secretary of Treasury designated as QOZ. These census tracks are located in all 50 states, including the District of Columbia, the US territories of America Samoa, Guam, Northern Mariana Islands, Puerto Rico and the US Virgin Islands. These designated census tracks expire in ten years and no later than December 31, 2028. The complete list can be found at the following site: https://www.irs.gov/pub/irs-irbs/irb18-28.pdf

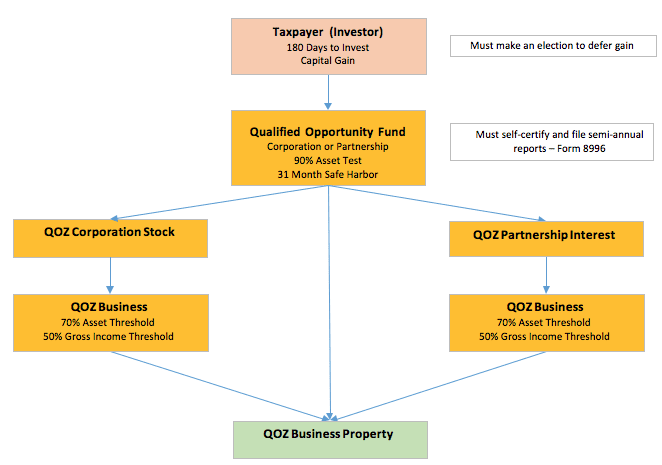

Quality Opportunity Funds are investment vehicles organized as a corporation or a partnership for Federal income tax purposes. The fund can be a partnership, a corporation or a limited liability company. The investor receives either stock or an equity interest in the fund. The fund must invest in Qualified Opportunity Zone Property, as explained below.

The QOF must hold 90% of its assets in a QOZ Property, measured both on the last day of the first six-month period of the taxable year of the fund and the last day of the taxable year of the fund. The QOF Form 8996 with the IRS semi-annually. Penalties will apply if the there is a failure to meet the 90% threshold.

QOF Safe Harbor – The proposed regulations provide a working capital safe harbor for QOF investments in QOZ Businesses that acquire, construct or rehabilitate tangible business property up to 31 months in which cash or cash equivalents qualify to meet the 90% asset test.

Investing in Opportunity Funds can provide the following incentives to investors:

- Deferral of capital gain;

- Possible reduction of the amount of capital gain realized through a basis adjustment;

- Possible permanent exclusion of capital gain on the appreciation for the interest in a QOF; and

- There is no cap on the amount of money that can be invested in QOFs.

To be eligible to elect the deferral of gain, the taxpayer (investor) must invest within 180 days of when the capital gain was recognized and must make an election under section 1400Z-2(a)(1)(A) for that tax year.

A QOF must be certified, which appears to be a simple process allowing taxpayers will be to self-certify as by completing and attaching Form 8996 to their tax return in the year they establish the QOF.

Qualified Opportunity Zone Property includes:

- QOZ Business Property, which represents any tangible property acquired after December 31, 2017 that is used in a QOZ Business; and either use of the property in the QOZ originates with the fund, or the fund substantially improves the property; and during substantially all of the QOF’s holding period for the property, substantially all of the use of the property was in a QOZ

- QOZ Stock, which represents any stock in a domestic corporation doing business as a QOZ Business that was purchased by the QOF after December 31, 2017, solely in exchange for cash, or in the case of a new corporation, such corporation was organized to be a QOZ Business.

- QOZ Partnership Interest, which represents any capital or profits interest obtained by the QOF after December 31, 2017, solely in exchange for cash, in a domestic partnership that is or will be formed to operate as a QOZ Business.

Qualified Opportunity Business is defined as a trade or business in which:

- Substantially all (at least 70%) of its tangible property, owned or leased, is QOZ Business Property;

- At least 50 percent of its total gross income is derived from the active conduct of its business;

- A substantial portion of its intangible property is used in the active conduct of its business;

- Less than five percent of the average of its aggregate unadjusted bases of the property is attributable to nonqualified financial property; and

- No portion of its proceeds is used to provide (including the provision of land for) any private or commercial golf course, country club, massage parlor, hot tub facility, suntan facility, racetrack or other facility used for gambling, or any store the principal business of which is the sale of alcoholic beverages for consumption off premises.

Additional Insight on Tax Incentive:

As mentioned there are major tax incentives to investors who reinvest in a QOF:

- The investor can elect to temporarily defer capital gains that they invest into a QOF until the earlier of:

– The date on which an investment is disposed, or

– December 31, 2026 subject to the 180-day period, or late June 2017. - The ability to preserve the exclusion of the post 10-year gain election, provided the disposition of the investment occurs prior to January 1, 2048.

- The permanent exclusion of 10% or 15% of the originally deferred tax

– If the investment is held for at least five (5) years, the investor will receive a 10% reduction in tax.

– If the investment is held for at least seven (7) years, the investor will receive a 15% reduction in tax. - The permanent exclusion of any gain attributable to appreciation in the QOF’s investment for those investors who hold their investment in a QOF for at least ten (10) years.

No additional election can be made with respect to a sale or exchange previously made unless the original investment into a QOF was completely disposed and then reinvested into another QOF. For example, if Mr. Jones sells property and realizes a gain of $500,000 and initially timely invests and elects to defer $300,000, he can no longer elect to defer the remaining $200,000. If Mr. Jones later sells or exchanges $150,000 of his original $300,000 investment, he will not be permitted to further defer the previously deferred gain on the sale or exchange, even if reinvested into another QOF. Mr. Jones would have to sell or exchange the entire $300,000 and then subsequently reinvest the entire proceeds into another QOF to continue to defer gain.

Based on the current program, we can expect, Mr. Jones, who sells property and realized a capital gain of $1,000,000 on June 30, 2018, who properly elects to defer the gain and invests the entire gain on July 31, 2018 (within the 180-day window) in a QOF, should realize the following results:

- After 5 years, Mr. Jones’ basis in his investment increased to $100,000 and after 7 years, Mr. Jones’ basis in his investment increased to $150,000.

- As of December 31, 2026, Mr. Jones will realize $850,000 gain and pay the taxes due ($1,000,000 – $150,000).

- Assuming that after 10 years, Mr. Jones’ investment appreciated to $2,500,000, he would recognize no gain from the sale. Assuming the original gain invested was subject to a 20% tax bracket, the total amount of tax paid on the $2,500,000 gain is effectively reduced to 6.8%.

The Flow Chart Below Illustrates Important Concepts In This Article

QUALIFIED OPPORTUNITY FUND

CONTACT US: The Treasury Department of the Internal Revenue Service continues to issue further guidance on this new incentive. If you have questions about the Investment Opportunity Act and the Qualified Opportunity Fund, contact Lou J. Fuoco, CPA at LFuoco@Fuoco.com or 561-209-1101.